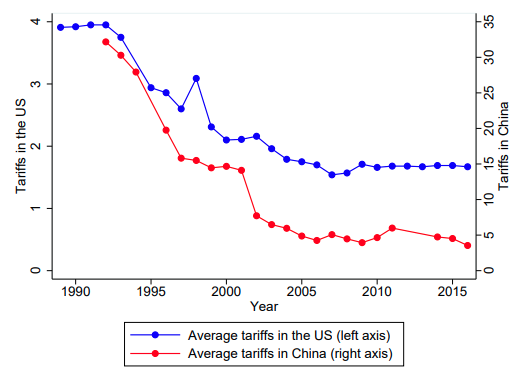

There’s been a lot of tough talk on trade lately. After tariffs (taxes imposed on imports) have fallen for decades (see Figure 1), there seems to be a shift in momentum and increasing appetite for raising rates again. Proponents (primarily President Trump) argue that this is vital for restoring US manufacturing. So far this summer, he’s issued three phases of tariffs against Chinese imports, and the Chinese government has responded to each in turn.

Figure 1. US and Chinese tariffs over time (Source: World Bank)

How is this going to affect the US economy, and especially the labor market? There’s a lot of talk (and a lot of speculation) on both sides of the issue, but at ZipRecruiter, we prefer to talk with data. So we turned to 12.5 million job openings posted since 2016 with a very simple question: How have the tariffs impacted hiring within the affected companies?

The evidence lines up behind an equally simple answer: Not much. We didn’t find any evidence of increased hiring among newly protected companies or decreased hiring among companies newly blocked from Chinese markets, and trust us, we looked pretty hard.

Below, we outline exactly what we did.

Background on the Tariffs

First, a quick refresher on the tariffs: Table 1 summarizes the five lists, issued between June 15 and July 11. Lists 1 and 2 announced US tariffs on Chinese goods (going into effect on different dates), which China responded to immediately with its own list of targeted US goods. A month later, the US issued List 3, which was by far the most comprehensive list yet (almost 8 times as many goods identified). China decided to respond by raising tariffs on the same goods that the US picked. If all five lists go into effect (four of which already have) a total of nearly 8,000 different products and $350 billion worth of trade will be affected between the two countries.

Table 1. Summarizing the tariff lists

| List Name | Tariffs On | List Size | Date Announces | Date in Effect |

|---|---|---|---|---|

| US List 1 | US imports from China | 818 goods ($34 billion in imports) | June 15 | July 6 |

| US List 2 | US imports from China | 284 goods ($16 billion in imports) | June 15 | August 23 |

| China List 2 | US exports to China | 545 goods ($34 billion in exports) | June 15 | July 6 |

| China List 2 | US exports to China | 114 goods ($16 billion in exports) | June 15 | August 23 |

| List 3 | Both | 6,031 goods ($200 billion worth of China-to-US trade, $50 billion worth of US-to-China trade) | July 11 | August 30 |

Where Do We Go From Here

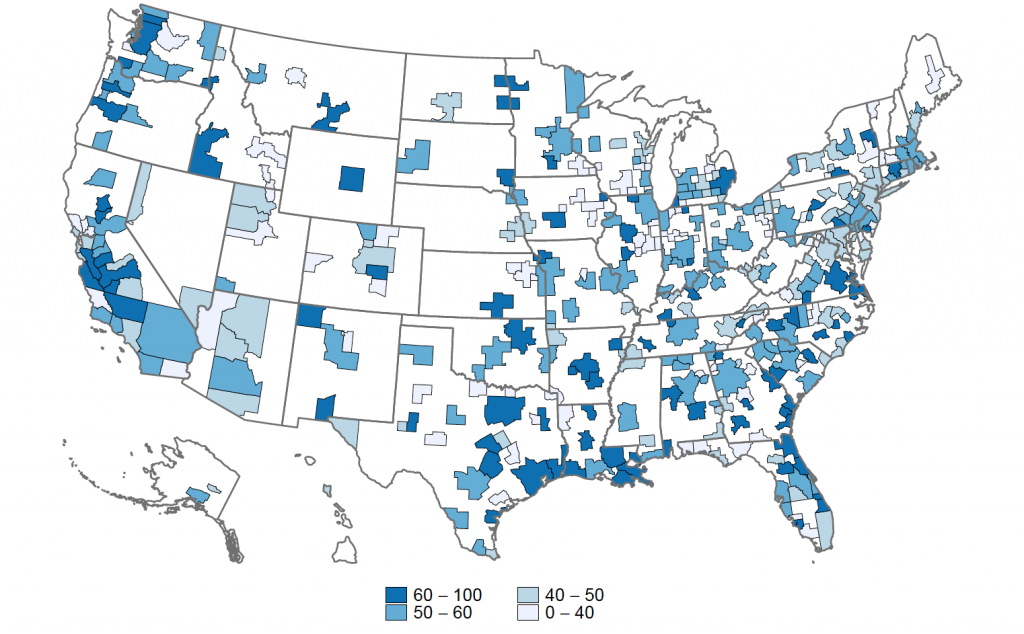

So these lists are a big deal, and lots of people are talking about them. So we thought it made sense to see whether businesses are already incorporating them into their hiring decisions. We built on a powerful insight of the recent trade research in economics: Different cities have different industries, and so they differ in their “exposure” to the effects of trade (recent review). We turned to one of the Census Bureau’s publications, the County Business Patterns, to figure out which metropolitan areas have the industries that appear on each of these 5 lists.

We calculated the share of each manufacturing industry’s products that appear on one of the lists, and the share of each MSA’s manufacturing employees who work in each industry. We can combine these to get a measure of each MSA’s “exposure” to the lists. We’ve included the gory details at the end for reference, but you can think of our “exposure” measure as the answer to the question: For the average manufacturing worker in this city, what share of the products he/she is making appear on the new tariff lists?

To see how this works, let’s talk about Wichita, Kansas, and Durham, North Carolina, as examples. Almost 60% of Wichita’s manufacturing workers produce Aerospace Product and Parts, and over 99% of those products showed up on these lists. Most of them were on List 3, which means that they see new tariffs on both imports from China (meant to protect US workers) and exports to China (which can hurt US workers). While many of Wichita’s other major manufacturing industries were spared, its heavy concentration in Aerospace means that roughly 75% of its manufacturing output was on the lists, and we calculate that it is a heavily exposed city.

Manufacturing in Durham is different. It’s a bit less specialized, so it takes four different industries to get up to 60% of its manufacturing workers, and those industries (Printing, Pharmaceuticals, Plastics, and Medical Equipment) were generally shielded. It’s biggest industry (Printing makes up 30% of Durham manufacturing employment) saw roughly a fifth of products appear on the list, and none of these industries saw more than a third of their products show up. Thus, we calculate that only about a quarter of Durham’s manufacturing output is affected by the new tariffs.

Figure 2 shows how 359 MSA’s around the country are affected by the lists. Darker colors mean a bigger share of products are affected. Across the country, there’s a pretty widespread. Every region (and most states) has both deeply affected metros (like Wichita, KS) and minimally affected metros (like Topeka, KS).

Figure 2. MSA-level exposure to the new lists

One quick clarification. You might be wondering why we’re lumping all the lists together. For instance, why not separate between industries seeing new US tariffs on Chinese goods and industries seeing new Chinese tariffs on US goods? In practice, because List 3 was so much bigger than the other lists, and every good on List 3 sees new tariffs on both imports and exports, there actually aren’t big differences between cities’ exposure to the Chinese lists and the US lists. In stats speak: The correlation between MSA exposure to Chinese tariffs and US tariffs is .94. In normal speak: Roughly 90% of goods seeing any change see both Chinese and US tariffs. (That said: We still tried to estimate different effects of the different lists, and it doesn’t change any of our results.)

So now that we know how exposed each MSA is, what do we do? We used an approach called “differences-in-differences” to estimate how the new tariffs affected openings that manufacturing companies posted to ZipRecruiter during the months before and after the change. The main idea is that we compare changes in posts before and after May 2018 (the first difference) across different cities affected differently (the second difference). This accounts for the fact that these MSA’s might be different from each other, and that some stuff is changing nationwide over time. We are, essentially, asking whether the change in manufacturing hiring this summer was different for more affected MSA’s compared to less affected ones.

What We Found

So what did we find? Nothing.

We don’t see any unusual increase or decrease in manufacturing hiring activity in the cities especially affected. The changes in hiring we see in very affected cities are almost identical to the changes we see in unaffected cities.

Doing statistics in the real world is always messy and never as precise as we’d like, but we really found no evidence at all suggesting an effect on hiring. It’s possible there’s some small increase or decrease, but our estimates can rule out that the tariffs had an effect of 10% or more.

But Really? Nothing?

Maybe there’s nothing comparing pre- and post-May, but we’d find something looking at later months? Nope.

Maybe there’s nothing on average, but we’d find something if we looked at the most heavily affected cities? Nope.

Maybe we’d find something if we look at cities that use ZipRecruiter more than others (that is, cities where our data might be more reliable)? Nope.

Maybe we’re mixing up increased hiring in cities affected by the new US tariffs, and decreased hiring in cities affected by the new China tariffs. We checked that. Nope.

Maybe only big companies (who understand complex tariff rules or are more likely to compete on international markets) respond more than small ones? Nope.

Conclusion

So has the recent round of China/US tariffs affected hiring among US manufacturers? No, at least not so far.

Why not? There are three potential explanations. First, maybe the effects will happen later. After all, most of the tariffs haven’t even been enacted yet. But we don’t think that’s it. Employers make hiring decisions by planning ahead, and thinking carefully about what (including access to foreign markets) is coming down the road.

For instance, from 1989 through 2001 (before China joined the WTO), Congress voted every year to give them an exemption from standard US trade policy by applying the very low WTO-member tariff rates to them anyway. But this was a vote that had to happen every year, and it was often pretty close, so no one could really plan ahead. When those rates became permanent, it had massive effects (summary here) because people could count on it. In other words, without changing the actual tariffs, changing expectations and plans alone massively disrupted the US labor market. Plans matter, and we don’t think that tariffs in place will have particularly different effects from tariffs in plans.

Second, maybe these tariffs didn’t have much effect because most industries saw new protection from China (US tariffs on Chinese goods) and restricted access to international markets (Chinese tariffs on US goods) at the same time. Maybe the effects offset.

We don’t really think that’s it either. When we use the small number of goods that saw only US tariffs or only Chinese tariffs, we tend to find the same thing (though admittedly it’s a little less clear, partly because this is a smaller sample). And it’s worth mentioning that trade between the US and China is massively imbalanced: We tend to buy much more from them than we sell. So you should think of even the goods getting both sets of tariffs as affecting Chinese producers more than US ones.

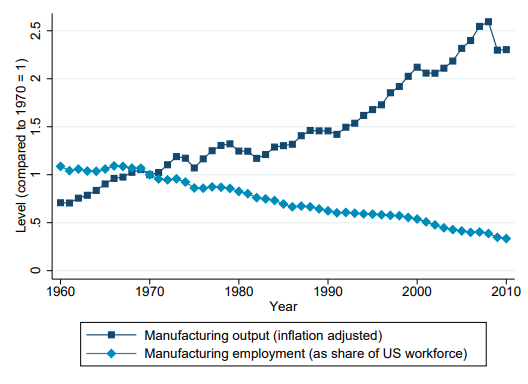

Third, maybe it’s because it’s hard to revive US manufacturing. We admit, that’s pretty controversial, but hear us out. Figure 3 shows something economists have been talking about for a long time. It presents US manufacturing output (adjusted for inflation) and employment (as a share of all US workers) from 1960 to 2010. Both are normalized to be 1 in 1970, so you can look at trends in both compared to that year.

Figure 3. Manufacturing output and employment over time (Source: Annual Survey of Manufacturing)

No one is doubting that China is important to US manufacturing. There’s a sharp drop in output starting right after they joined the WTO in 2001, and the decline of manufacturing employment does accelerate from there on. But the figure shows that blaming rustbelt workers’ or blue collar workers’ woes on China misses a big part of the story. From 1970 to 2000, manufacturing output increased by 112% while employment fell (that’s right, fell) by 45%. The story of US manufacturing over the last 50 years is making more with fewer workers. There are many potential explanations for this, but even if tough tariff policy can bring us back to an America before massive Chinese imports (which remember, was only 25 years ago), it’s not going to be so easy to restore manufacturing employment to “the golden days.”

Technical notes

We took this analysis pretty seriously, and applied a lot of standard statistical procedures to make sure we were doing things right.

All regressions include MSA and month fixed effects, and weight by total MSA employment so that our results are representative of the US workforce. All use the natural logarithm of the number of manufacturing openings posted in the MSA during the month.

For our primary measure of an MSA’s exposure, we calculate the share of all products (8-digit HS codes) in a manufacturing industry (6-digit NAICS codes) that appear on one of the lists. We then calculate a weighted average across industries, where the weights are the industry’s share of all manufacturing employment in the MSA. We can use weights based on the industry’s share of all employment (including non-manufacturing) and we get the same results.

You might worry that tariff-affected and unaffected places are pretty different than places we presume are unaffected by tariffs. To make sure that we were comparing apples and orange, we used standard trimming methods to ensure that highly exposed Metropolitan Statistical Areas (MSA’s) and minimally exposed MSA’s had overlapping support in the distributions of total MSA employment, as well as growth in manufacturing posts during the run-up to the tariffs.

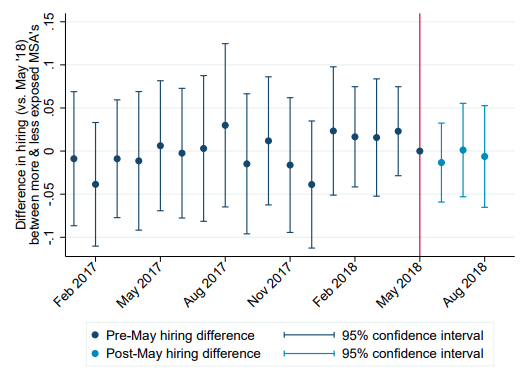

How do we know that more exposed and less exposed MSA’s are similar to each other? We checked. Figure 4 shows the estimated coefficients from generalized difference-in-difference specification. The standard thing that economists want to see to ensure that you’re comparing apples and apples is that the “treated” and “control” MSA’s have similar hiring trends leading up to the event. You can see that in the navy blue estimates to the left. They fluctuate around zero, suggesting that more and less exposed MSA’s saw similar hiring patterns prior to May 2018. This means they’re a pretty good control group. Then the bright blue estimates on the right, also fluctuating around zero, show that more and less exposed MSA’s kept hiring at similar rates afterwards. This means, the tariffs haven’t affected hiring.

Figure 4. The nitty-gritty estimates themselves

If you’re still sitting there thinking “correlation doesn’t equal causation” and wondering whether we’re really doing a fair analysis, we employed a triple-difference approach, where the third difference (in addition to over time and across MSA’s) is between hiring in manufacturing and outside of manufacturing. For this analysis, we are essentially checking whether manufacturing hiring changed in a different way from other types of hiring. It did not. We get the same answer.

And if you’re a real technical stickler, you might worry about using the natural logarithm being undefined when there are no posts. This rarely happens, and even less if we drop very small MSA’s (which doesn’t affect the results). We can also use the inverse hyperbolic sine transformation, and that doesn’t affect our results either.

Why couldn’t you do this analysis with BLS data? Do we need ZipRecruiter data? Yes. The Current Population Survey only identifies 260 MSA’s, roughly two-thirds of how many we can look at with ZipRecruiter data. Moreover, the CPS includes only 60,000 respondents per month, whereas we see around 400,000 openings per month. And it’s actually worse than this when you consider that only around 2.6% of workers in the CPS are newly hired – meaning that it only captures around 1,500 new hires per month.