When unemployment is this low (a record 3.7%), and job openings outnumber active job seekers, wages tend to rise. But over the past few years, average wage growth has been sluggish—even when you use the rosier wage-growth measure suggested by the White House.

We are finally beginning to see some better wage growth numbers. According to the October 16 data release from the Bureau of Labor Statistics, weekly earnings were up 3.3% in the third quarter of 2018 YoY—enough to pay for a 2.6% increase in the CPI, and give workers a 0.7% real increase. But the quarterly real wage series is quite volatile, and the bigger picture is two years of essentially flat earnings.

1. Variation in Labor Supply Across Occupations

Just as matter is subject to gravity, prices are always and everywhere subject to the vagaries of supply and demand. But observers may not fully appreciate the extent to which labor supply differs across occupations.

- In occupations with low skill requirements and relatively pleasant working conditions, many people are able and willing to fill vacancies, and employers can meet their hiring targets without raising wages.

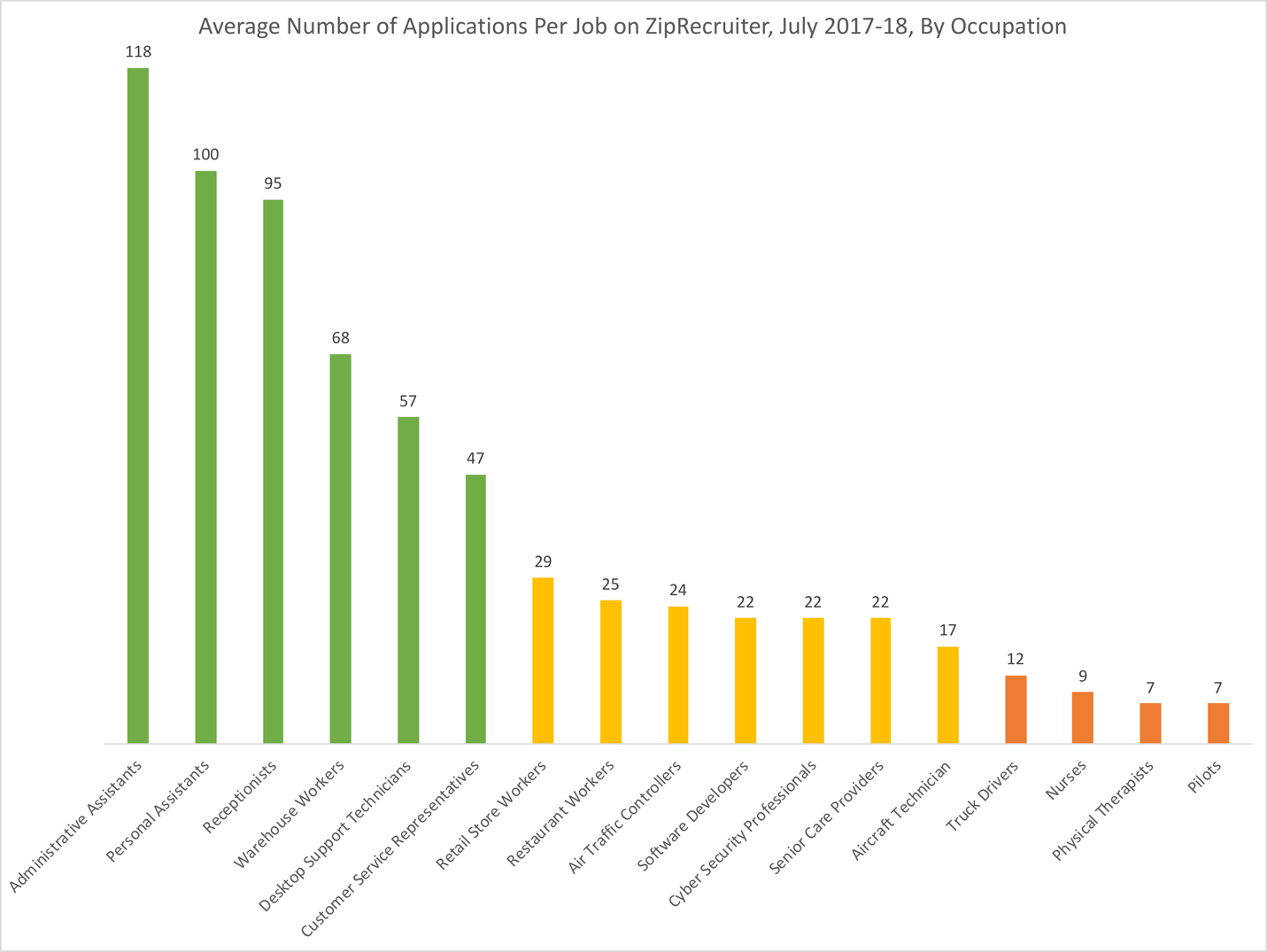

ZipRecruiter data shows that in occupations with low training requirements and pleasant job conditions, the number of applications per job posting tends to be very high. For example, over the past year, there were 118 applications per job on average for administrative assistants and 95 for receptionists. In these occupations, employers have plenty of candidates to choose from, and don’t feel much pressure to raise wages.

From a job seeker’s perspective, getting a job as a receptionist or administrative assistant can be harder than getting into Harvard, with its relatively generous 4.6% acceptance rate! Unsurprisingly, then, the latest occupational earnings data from the Bureau of Labor Statistics show that median earnings for administrative assistants and receptionists are increasing by just 1.7%, below the rate of inflation.

- In other occupations that require specialized skills and many years of training—or that are dangerous and difficult—there are far fewer people qualified or willing to do the job. When training pipelines are long or occupational licensing requirements are onerous, raising wages may not be very effective at boosting the number of qualified candidates.

There were just 12 applications per truck driving job and 7 per pilot job on average on the ZipRecruiter platform over the past year, and median earnings in those occupations are increasing much more quickly—at 2.8% for truck drivers and 5.9% for pilots. There were also shortages of qualified candidates in nursing and physical therapy.

Source: ZipRecruiter data, author’s calculations

2. Surprisingly Slow Productivity Growth

Another important factor affecting wage growth is the productivity growth rate (i.e. how quickly output generated per worker-hour is increasing). Despite voice-driven computing, digital cloud-based services, 3D printing, and other technological innovations, the rate of productivity growth has been very low over the past decade.

Productivity and wages grew in tandem between 1940 and 1970, but since then, wages have grown more slowly than productivity, for a number of reasons. In other words, it could take a substantial boost in productivity before we see a modest increase in real compensation.The good news is that many observers think this is merely the calm before the productivity storm. While recent innovations may have been less transformative than some that came before—clean water, electricity, the internal combustion engine, petroleum, powered flight, air conditioning, telecommunications—super computing power, big data, and artificial intelligence may be on the brink of sparking a productivity explosion as they diffuse more widely through the economy.

3. Sticky Wages

Sometimes workers’ earnings don’t adjust quickly with supply, demand, and productivity, as John Maynard Keynes famously noted in his General Theory of Employment, Interest, and Money. Wages, Keynes observed, are sticky on the way down. It turns out workers like nothing less than a wage cut. During the Great Recession—as during the Great Depression 75 years earlier—companies on the brink of bankruptcy were more likely to lay off or furlough 20% of their workers than they were to cut salaries by 20%.

- The flipside of wages being sticky on the way down, is that they can be sticky on the way up as well. Companies recall how they struggled to make payroll during the Recession, and are therefore reluctant to raise wages now, lest they make it harder for themselves to weather the next downturn.

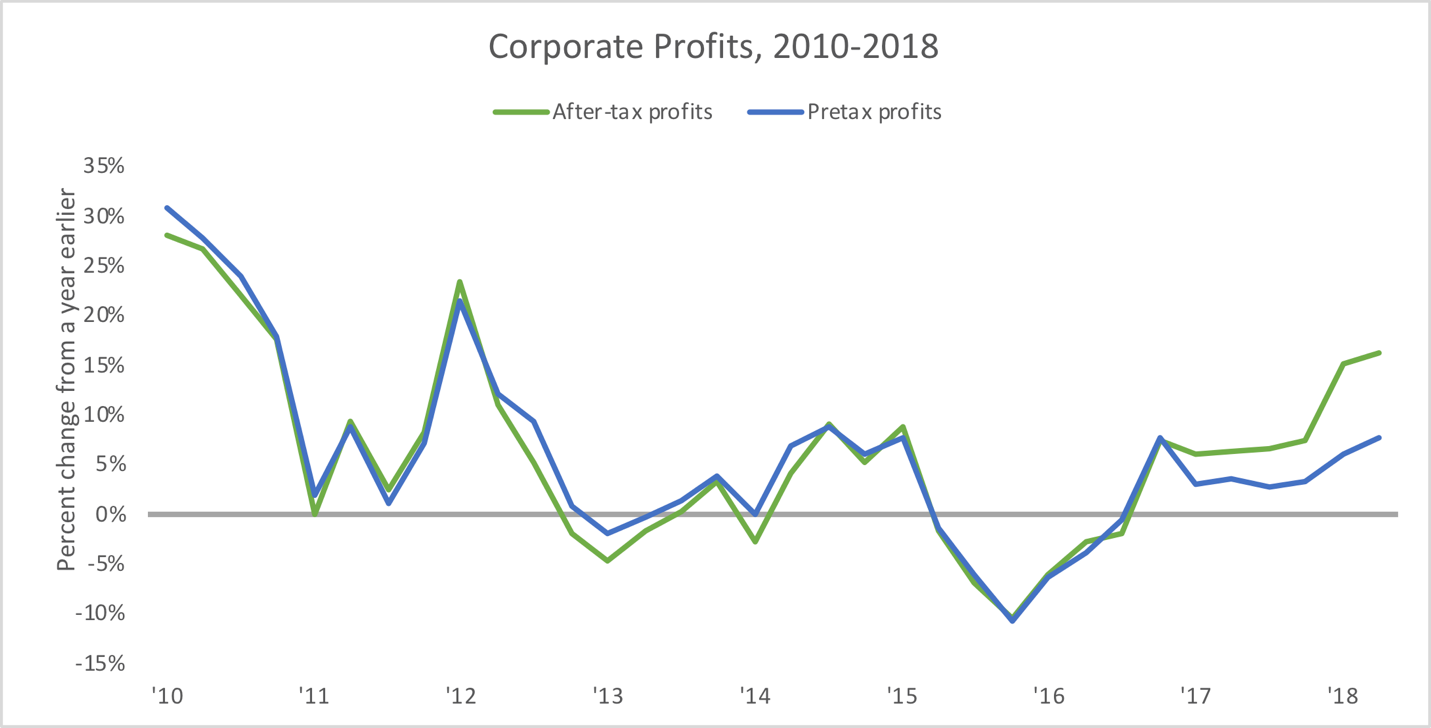

Many firms are behaving very cautiously because they are over-leveraged. The economic recovery depended on the Federal Reserve reducing interest rates and taking drastic measures to make credit available to businesses that needed it. As a result, corporate debt levels are still very high. Corporate profits have soared since late 2017, so there’s a good chance firms may soon feel more confident about raising wages. But these decisions don’t happen overnight.

Source: U.S. Commerce Department

Worker expectations may also contribute to recent wage rigidity. Many workers lost their jobs during the Great Recession or saw friends and family members lose theirs—and not just blue-collar workers. With that memory still so fresh, many workers are just grateful for a job. Some are reluctant to ask for raises, lest they become too expensive to their firms and find their heads on the chopping block in the next downturn.

John Grisham’s novel, Gray Mountain, tells the story of Samantha Kofer, a super-achiever Ivy League graduate at a huge Wall Street law firm, who is on track to earn a quarter of a million dollars a year, but then gets furloughed and escorted out the building when the recession hits, and offered the opportunity to work at a legal aid clinic without any pay at all. Samantha’s story is the story of a whole cohort of bright young Americans whose earnings expectations were smashed by the Great Recession—and, in many cases, have yet to recover. Studies find it can take 10 years for the earnings effects of a recession to recede. In a recent ZipRecruiter job seeker survey, 23% of respondents said that the they were lowering their salary expectations in order to increase their chances of getting a job.

4. An Aversion to Unpleasant Jobs

Another factor behind low wage growth is the decline in geographic mobility and job-to-job mobility. But this may not be a bad thing. People uproot their families when induced to do so by sufficiently awful conditions, such as discrimination, physical violence, and economic hardship. Think of the African American Great Migration north between 1910 and 1970, or the Jewish exodus from Europe between 1914 and 1948, or more recent migration to Europe from war-torn countries in the Middle East. As U.S. households become more prosperous and poverty rates fall, it should come as no surprise that people are increasingly happy to stay put.

What is surprising, however, is the extent to which people avoid unpleasant jobs when the economy strengthens. When the economy is weak, companies have to do more with fewer staff, and workers—who increasingly struggle to find jobs or keep them—are increasingly likely to accept night shifts and otherwise unpleasant or dangerous work. For example, drivers are more likely to add tank and hazardous materials endorsements to their commercial driver’s licenses in a contracting economy. (Transporting dangerous loads is riskier and more likely to attract unwanted attention from law enforcement officials, but it allows drivers to bid on a wider range of jobs, which is particularly valuable when jobs are scarce.) Difficult jobs tend to pay more per hour to compensate workers for the undesirable conditions, but when workers have a choice, a recent study finds, they systematically move to lower-paying firms offering more pleasant work.

5. A Switch in the Distribution of Wage Growth Gains

One final reason for low average real wage growth was recently highlighted by former chair of the Council of Economic Advisers, Jason Furman: Current wage growth is surprisingly slow at the top of the wage distribution, and fast at the bottom. Due to the mathematics of averages, changes in the earnings of the wealthy have an outsized influence on the average wage. During the late 1990s, real average hourly earnings grew at rates between 1% and 2% per year for workers in the bottom four quintiles, but at almost 3% per year for workers in the top quintile. When someone earning $1 million gets a 3% (or $30,000) raise, that pulls up the overall average wage far more than when someone earning $30,000 gets a 5% (or $1,500) raise. In other words, the rapid rise in average wages in the late 1990s was largely driven by growth at the top.

Furman points out that in the past three years, by contrast, “workers in the bottom two-fifths of the income distribution have seen comparable or faster real wage growth than they did in the late 1990s. Higher earners, meanwhile, have seen much slower wage growth than they did in the 1990s.”

Just like the reduction in geographic mobility, the shift in the distribution of wage gains may not be a bad thing. In fact, it may be a sign of health. As falling ratios of unemployed workers to job openings affect a wider range of sectors, as the diffusion of newer technologies across industries unleashes productivity gains, and as expanding employment raises worker expectations, upward pressure on wages will finally build.

Employers may have little choice but to provide employees with that long-awaited raise.